Online Marketplace Businesses

Marketplace businesses offer one of the most durable competitive advantages available in the business world: network effects. The best marketplaces deliver value to all parties involved in the transaction (often creating Money Out of Nowhere) and have very attractive financial profiles (often experiencing increasing returns to scale). Unsurprisingly, many marketplace businesses have been excellent investments.

To ascertain the existence of network effects, ask the following question:

Can the marketplace provide a better experience to customer “n+1000” than it did to customer “n” directly as a function of adding 1000 more participants to the market?

Hamilton Helmer contends that competitive advantages must confer both a benefit to the business and a barrier to the business's competitors. Ideally, though, the competitive advantage will confer a benefit to customers, too.

This is one area where network effects shine: the larger the network, the more value there is for an incremental user.

Think of eBay or Etsy: the more buyers there are on the platform, the more valuable it is for a seller, and vice versa. These businesses don't have to lower prices in order to increase the value that all parties receive. Greater selection provides a benefit to buyers automatically. Likewise, the company doesn't have to offer better take-rates for their suppliers, since more buyers result in more revenues and more profits for their suppliers.

While other competitive advantages like brand and scale can result in benefits to customers if the management team constantly pushes the business to improve the customer value proposition, network effects are unique in that, by their very nature, they naturally confer greater & greater benefits to customers as the business scales and the network-effect-based flywheel spins. Management teams need only nudge their business in the right direction, rather than heave their business in that direction (it takes a great deal of heaving to get the flywheel spinning to begin with).

Of course, marketplaces must curate the offerings to a degree - for example, Tinder and other dating apps allow users to search by age and geography (if they didn't then the larger these apps became the less useful they'd be as search costs for your ideal mate would create greater & greater friction for users e.g. someone in London is unlikely to benefit from seeing someone's profile from North Carolina and vice versa).

Online marketplaces are often high quality businesses due to network effects, but what can make them great investments is their attractive financial characteristics.

John Huber explains:

[Network effects] when combined with a marketplace business model, [can result in] a toll road, taking a high margin royalty on the commerce that happens on its platform. They usually have very attractive economics with low capital requirements and often little to no marginal costs, which means expanding profitability as the business grows. But the most important feature of a true network is that it gets stronger as the business grows. Network effects defy the nature of capitalism - profit margins expand while simultaneously becoming harder for competitors to attack.

Growth generated by online marketplaces is done with little incremental invested capital by the marketplace businesses themselves.

Here's Huber again, on the topic of "growth from others' capex":

Merchants pay to make stuff and have to fund their own inventory, shippers build the distribution networks and buy the trucks, but the companies processing the payments earn most of the profits that come from that aggregate invested capital. Adyen is now larger than Spotify, a big early customer, which is itself more valuable than many of the labels which own the content that Spotify distributes. You can see who reaps most of the value in that ecosystem, and who is funding the ecosystem's growth. The returns on invested capital are not distributed proportionately. Similarly, PayPal was once a minnow in eBay's ocean, but PYPL now has a market cap nearly 8x the size of its former parent.

A big reason why PayPal became so valuable is it could grow using other people's money.

Microsoft's growth was funded by IBM's investments. Facebook's growth was funded in part by telecoms' broadband investments.

As Buffett says, the best business is a royalty on the growth of others.

While the marketplace bears upfront, fixed costs (such as the costs of software development as well as general & administrative expenses, neither of which are ever completely 'fixed' in the long-run), the marketplace's suppliers bear most of the invested capital costs. Furthermore, distribution is free over the internet and the suppliers pay the COGS, so marginal costs are often minimal, resulting in high incremental margins (aka contribution margins). Marketplaces own the demand, and outsource the supply.

When a business with contribution margins above its historical profit margins can grow its revenues faster than it grows its fixed costs, then profits grow faster than revenue. Profit margins trend towards contribution margins over time. This financial characteristic, called 'operating leverage', is not unique to online marketplaces. However, operating leverage is visible at many successful marketplaces, as are high returns on incrementally invested capital. As Huber points out, these businesses grow on the back of other companies' capex.

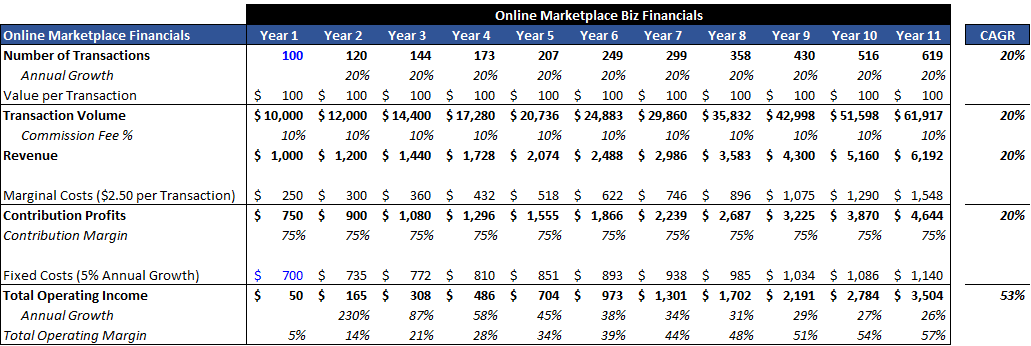

Let's demonstrate this with a fictional online marketplace business that grows revenues at a 20% CAGR over 10 years. Due to incremental margins of 75% vs Year 1 operating margins of 5%, operating income (a proxy for FCF) grows by a stunning 53% and operating margins rise from 5% to 57%, steadily approaching its asymptote of 75% (i.e. the business's incremental margins).

The greater the differential between historical profit margins and incremental contribution margins, the faster the business will grow profits for any given level of revenue growth. Operating income grows at 36% from years 3 - 11 vs 53% growth from years 1 - 11, because the starting operating margin is 21% in year 3 vs 5% in year 1 (and revenue growth is 20% every year in this example).

It's also worth noting that customer acquisition costs can actually decrease over time with marketplaces, as the larger the network the more value customers derive from it and thus less 'convincing' is required to get customers to join the marketplace. Normally customer acquisition costs increase over time.

A lot of smart people have written great posts/given great talks on the topic of online marketplace businesses. It’s hard to add much to the conversation given how much ink has been spilt already. The remainder of this post is my attempt to curate the best of what other people have already written/spoken:

- Bill Gurley’s: Ten Factors to Consider When Evaluating Digital Marketplaces; Money Out of Nowhere: How Internet Marketplaces Unlock Economic Wealth

- NFX’s “Network Effects Manual”

- Y Combinator on “Network Effects”

- A16Z: Marketplaces video; All About Network Effects; 16 Ways to Measure Network Effects; The Dynamics of Network Effects

- Sarah Tavel’s Hierarchy of Marketplaces: Part 1; Part 2; Part 3

- Ben Thompson on Aggregators vs Platforms: Landing page; Aggregation Theory; The Bill Gates Line; talk at Recode 2018

- Everything Sameer Singh has written at Breadcrumb.vc

- Hamilton Helmer’s book ‘7 Powers’ has a chapter on network effects that is fantastic

- John Huber's post 'The End of Mean Reversion'

- Connor Leonard on ROIC and 'Reinvestment Moats' as well as his follow-up post on Capital-Light Compounders (these posts aren't exclusively about online marketplaces, but touch on the concept)

- My post on Network Health

An interesting trend we're seeing more & more of is software businesses, who've historically benefitted from switching costs & economies of scale, offering marketplaces as a core part of their value proposition to customers. Obviously Amazon did this years ago with Amazon Marketplace, but now we're seeing it with software companies such as Coupa, Guidewire and Square (to name just a few). When you can combine network effects with other competitive advantages, you can be in for a real lollapalooza outcome.

If you’re reading this and feel like I’ve missed your post/talk or a great post/talk by someone else then please email me – I’d love to hear from you.